Market Recap / Conditions:

General Commentary:30/03/2026

On day 30 of the conflict, tensions escalated further as Houthi rebels from Yemen joined Iran in the battle, raising the risk of a broader regional war. This development is particularly significant for global energy markets, as the Houthis have the capacity to disrupt key shipping routes in the Red Sea, especially the Bab el-Mandeb Strait, through which roughly 10% of global seaborne oil trade passes. Any disruption in this corridor would place additional pressure on already strained supply chains and energy markets. US equity markets continued to weaken over the month, with the S&P 500 down 7.45%, the Nasdaq down 7.44%, and the Dow falling 7.6%. The US has extended its infrastructure bombing deadline to 6 April, while the Pentagon is reportedly considering deploying up to 10,000 troops, signalling preparations for a potentially longer conflict. On the domestic front, sentiment has deteriorated sharply, with the University of Michigan Consumer Sentiment index falling to 53.3, near record lows, while year-ahead inflation expectations jumped to 3.8%, marking the largest monthly increase since April 2025. Energy markets responded strongly, with Brent crude up 4.22%, gasoline up 3.83%, and heating oil rising 5.2% on the day. In China, authorities have opened a trade probe against the US in retaliation for tariffs, adding another layer of geopolitical tension. Meanwhile, in Australia, the RBA has signalled that further rate increases are likely.

As there is so much topical news again this week’s Buzz is broken into 2 parts: potential concerns over Houthi rebels joining Iran and we take a brief look at the domestic situation with a focus on the RBA’s decision to increase rates and what this should mean for the ASX200 and the AUD.

But first, the conflict between the US and Iran has expanded beyond a bilateral war into a broader regional confrontation, with Iran-aligned groups such as the Houthis now entering the fight and increasing risks to key shipping routes. Iran is not backed by a single formal alliance, but instead relies on a network of proxy groups and limited support from major powers. Its strongest backing comes from Iran-aligned militant groups across the Middle East—often referred to as the “Axis of Resistance”—including Hezbollah in Lebanon, Hamas and other Palestinian groups, and Shia militias in Iraq and now openly the Houthis in Yemen. These groups are funded, trained, and equipped by Iran and effectively act as extensions of its influence, allowing it to operate across multiple fronts. At the state level, support is more indirect: Russia provides strategic and military assistance, while China offers economic and diplomatic backing, particularly through energy trade. However, most major regional powers, such as Saudi Arabia, the UAE, Egypt, and Turkey, do not support Iran and are generally aligned with Western interests. Overall, Iran’s strength lies in its ability to project power through this decentralised network rather than through traditional alliances, and this is one reason why we feel the US have miss judged the incursion.

Despite sustained US strikes, Iran retains significant military capability, with only part of its missile arsenal degraded, suggesting the conflict is far from resolved from its perspective. While the US has indicated a preference for a short campaign, ongoing troop deployments and contingency planning point to preparation for a more prolonged engagement.

The situation has further escalated with the involvement of the Houthi rebels in Yemen, raising the risk of disruption to key shipping routes in the Red Sea. In particular, the Bab el-Mandeb Strait—through which approximately 6–7 million barrels of oil per day flow, or around 10% of global seaborne trade—remains a critical chokepoint and gateway to the Suez Canal. Any disruption here would place additional pressure on already strained global trade routes and energy supply chains. At the same time, the nearby Strait of Hormuz remains constrained, with around 20–21 million barrels per day—roughly 20% of global consumption—at risk. Taken together, the region accounts for close to 30% of global oil supply, meaning any escalation carries significant implications for energy markets.

Importantly, the key constraint is not only whether vessels can physically transit these routes, but whether they can secure war-risk insurance. Without adequate coverage, many ships will be unwilling or unable to pass, effectively restricting supply regardless of access. Reflecting these risks, energy markets rallied strongly over the week, while equity markets declined sharply.

The conflict is having an inflationary impact primarily through the energy channel, with disruptions and heightened risk around key chokepoints such as the Strait of Hormuz and Bab el-Mandeb driving oil and fuel prices higher. This feeds quickly into transport, electricity, and broader production costs, lifting headline inflation. Higher shipping and insurance costs are also increasing freight rates, which in turn raises the price of imported goods, food, and manufacturing inputs. As businesses face rising input costs, these pressures are typically reflected first in producer prices before being passed through to consumers, contributing to sustained inflation. At the same time, higher costs are weighing on economic growth, creating a stagflationary dynamic where inflation remains elevated even as demand weakens, complicating the outlook for central banks and interest rate policy.

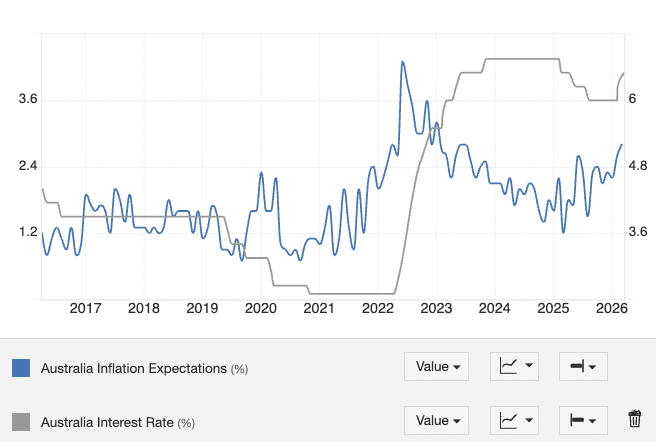

The conflict has made the RBA’s outlook more complex and tilted toward a higher-for-longer stance. While inflation had been moderating, the surge in energy prices and shipping costs is now reintroducing upside risks, particularly through fuel, transport, and broader input costs. Pushing inflation expectations to levels not seen since Jun 23. This places the Reserve Bank of Australia in a difficult position, as inflation expectations are increasing and will be sustained whilst the war continues, whilst official interest rates have not normalised since the pandemic and are relatively high retrospectively at 4.1% and by all accounts, the Governor has indicated will go higher if inflationary pressures as a result of the war persist.

From a market perspective, this environment is bearish for the ASX 200, as higher interest rates, rising input costs, and weaker consumer sentiment weigh on earnings and valuations. Equity markets are particularly vulnerable to further downside as the full economic impact of the conflict is priced in.

For the AUD, the outlook is more nuanced but increasingly constructive. In the near term, the currency may remain under pressure due to a flight to safety into the US dollar. However, once this risk-off dynamic subsides, the Australian dollar is likely to turn more bullish, supported by interest rate differentials between Australia and the US, particularly if the RBA maintains a tighter stance while US policy expectations begin to ease. Combined with Australia’s exposure to commodities, this could provide a stronger medium-term foundation for the currency.

The risk of Australia entering a recession is rising due to several key factors. Higher energy prices are increasing fuel, transport, and business costs, effectively acting as a tax on the economy and reducing household spending power. At the same time, the RBA is likely to keep interest rates higher for longer, which places additional pressure on highly leveraged households, lifting mortgage stress and slowing consumption. Consumer sentiment is already weak, and rising living costs are further reducing discretionary spending, weighing on sectors such as retail and services. In addition, global growth risks are increasing due to the conflict and energy shock, with particular concern around China’s economic outlook, which could reduce demand for Australian exports and dampen overall economic activity.

Markets will remain focused on signs of de-escalation in the Middle East, particularly as the US has delayed further attacks into the coming week, while the halt in Persian Gulf exports continues to pose a risk to global growth. In the US, a shortened trading week due to Easter will still feature key data, including the jobs report and ISM Manufacturing survey, which will provide insight into the impact of higher energy costs on economic activity. In Europe, attention will turn to the Eurozone’s first inflation reading since the start of the conflict, highlighting the pass-through of energy prices. China will release both official and broader PMI data, offering an early look at how the world’s largest energy importer is responding. Meanwhile, monetary policy updates are expected from the Bank of Japan, Reserve Bank of Australia, and Bank of Canada.

We have re-entered long oil positions and are currently holding them cautiously given the heightened volatility. On the currency front, we remain long AUD/USD and AUD/CHF; however, both pairs have come under pressure as investors rotate into the US dollar as a safe haven. We expect this dynamic to reverse over time as capital is repatriated and USD strength fades. In addition, the interest rate differential between the US and Australia is increasingly supportive of the AUD, making it more palatable to maintain these positions.

We have also re-entered positions in gold and silver, expecting their safe-haven characteristics to support prices, despite recent volatility. On the equity side, we have taken some profits but continue to hold a core short bias as we assess the broader market implications of the conflict. We also maintain our long position in wheat.

Trade Focus:

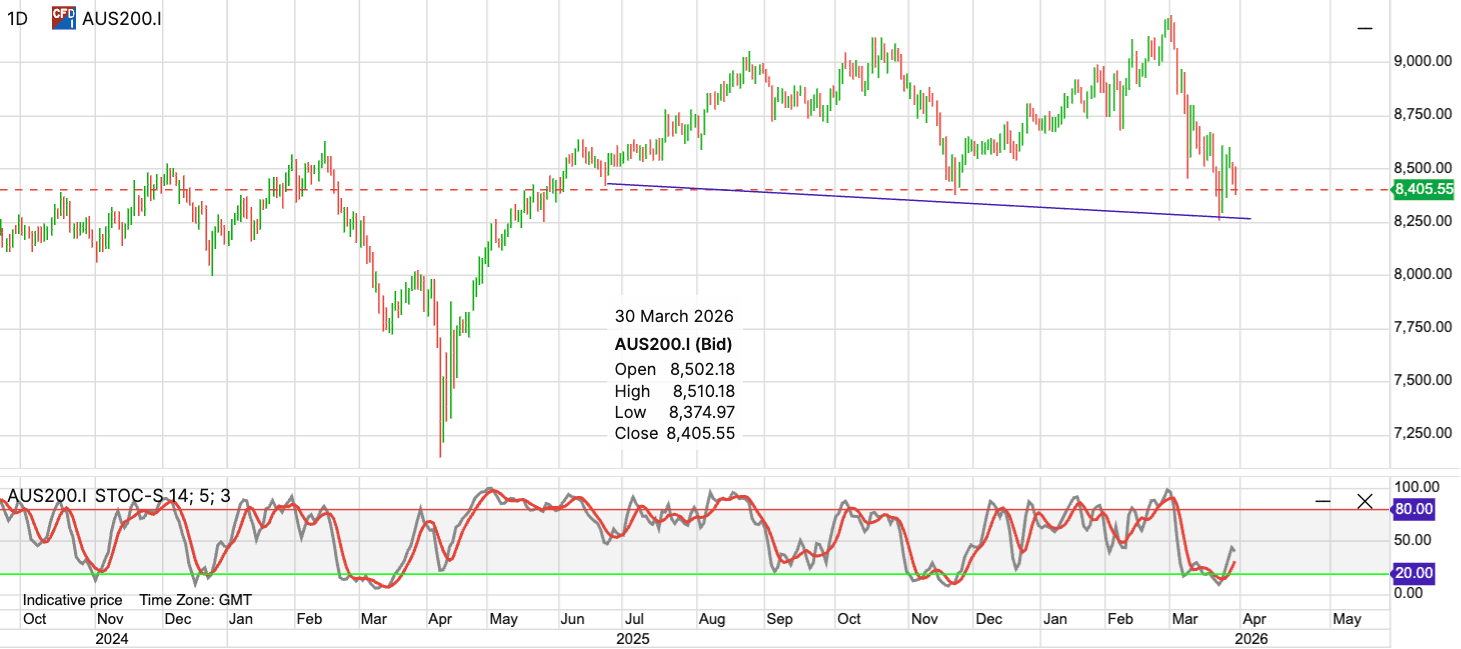

ASX200

Fundamentals:

The outlook for the ASX 200 remains bearish in the near term, and as mentioned above, is driven by a combination of higher-for-longer interest rates, rising input costs, and weakening consumer demand. Elevated energy prices are adding pressure to margins across key sectors, while tighter financial conditions continue to weigh on valuations. At the same time, global uncertainty and slowing growth—particularly in China—are likely to dampen earnings expectations. With sentiment deteriorating and macro risks building, the ASX is vulnerable to further downside as markets continue to price in a more prolonged and uncertain economic environment.

Technical Analysis:

The ASX 200 is currently showing a bearish technical structure, with price action trending lower and failing to hold key resistance levels. The index has broken below prior support zones 8500, which are now acting as resistance, reinforcing downward momentum. Short-term moving averages have rolled over and are trading below longer-term averages, signalling a negative trend bias. Momentum indicators such as the Stochastic and RSI are sitting in lower ranges, indicating weak buying pressure but not yet deeply oversold conditions, suggesting there may still be room for further downside. A sustained move below recent support levels, 8250 would likely accelerate selling pressure, while any recovery would need to reclaim key resistance zones, 8500 to shift sentiment. Overall, the technical setup points to continued weakness unless a clear reversal signal emerges.

Disclaimer:

ETO Markets, the trading name of ETO Group Pty Ltd (ABN 66 155 680 890), is a financial services company regulated by the Australian Securities and Investments Commission (ASIC) under AFSL No. 420224. If this email contains reference to any financial products, ETO Markets recommends you consider the disclosure documents available from us before making any decisions regarding any products. The contents of this email (including any attachments) are confidential and may contain privileged information. Any unauthorised use of the contents is expressly prohibited. If you have received this email in error, please notify us immediately by email and then destroy the email and any attachments or documents.

Before making any investment, decision or starting any transaction, you need to carefully consider your current financial situation and consult your financial advisor to understand the potential possible risks to confirm whether you are suitable for such investment or transaction.

The above information will not be reproduced or used by anyone in any country or jurisdiction. Any reprint or use will be deemed illegal. The opinions expressed in the above information are subject to change without notice.