ETO Markets Weekly Recap / Conditions:

US equity markets advanced as investors reacted positively to comments from Federal Reserve President John Williams, who suggested that monetary policy may soon shift toward a more neutral stance. This helped push the implied probability of a December rate cut back up to nearly 70%, lifting market sentiment despite continued signs of strain across the broader economy. Gold prices trimmed earlier losses to finish around US$4,080, supported by the ongoing release of delayed economic data following the recent government shutdown. Labour market figures reflected a gradual cooling, with non-farm payrolls rising by 119,000 while the unemployment rate edged higher to 4.4%. Although jobs growth remains positive, momentum has slowed, reinforcing expectations that tighter policy is working its way through the economy. Weakness also emerged in manufacturing, where the latest PMI reading slipped to 51.9 — the softest level in four months — indicating fading industrial activity as demand moderates. Consumer confidence continues to deteriorate sharply. The University of Michigan Consumer Sentiment Index dropped to 51.0, its second-lowest reading on record, while the Current Economic Conditions Index plunged 12.8% to a new all-time low of 51.1. These figures highlight mounting household concerns over inflation, employment prospects, and financial security. Minutes from the most recent Federal Reserve meeting further revealed a deeply divided committee, reflecting a challenging policy environment where inflation progress remains uneven. In commodities, oil fell 2% to US$57.50 per barrel after remarks from Ukrainian President Volodymyr Zelenskiy signaled openness to exploring peace talks — raising hopes for reduced geopolitical tension and easing supply-risk premiums.

Although equities saw a small rebound on Friday, markets still finished the week in negative territory. The S&P 500 declined -1.95%, the Dow Jones slipped -1.91%, and the Nasdaq 100 led losses with a -3.07% fall, reflecting ongoing pressure on growth and technology stocks. Global markets also struggled to gain traction.

With the US Government now fully operational again, this week’s Buzz will take a deeper look at the backlog of delayed economic releases and question whether the latest data supports the case for a Federal Reserve rate cut at the upcoming meeting. These insights will also help determine whether we maintain our bearish stance on US equities, given persistent economic headwinds, weakening sentiment, and elevated earnings expectations.

US financial markets continue to grapple with a mixed and increasingly fragile economic backdrop, where improving inflation dynamics are being offset by deteriorating consumer confidence and signs of strain across the industrial and retail sectors. With the federal government now fully reopened and official data flows resuming, investors have turned their attention back to incoming economic indicators, searching for clarity on growth momentum and the Federal Reserve’s policy trajectory heading into the final stretch of the year.

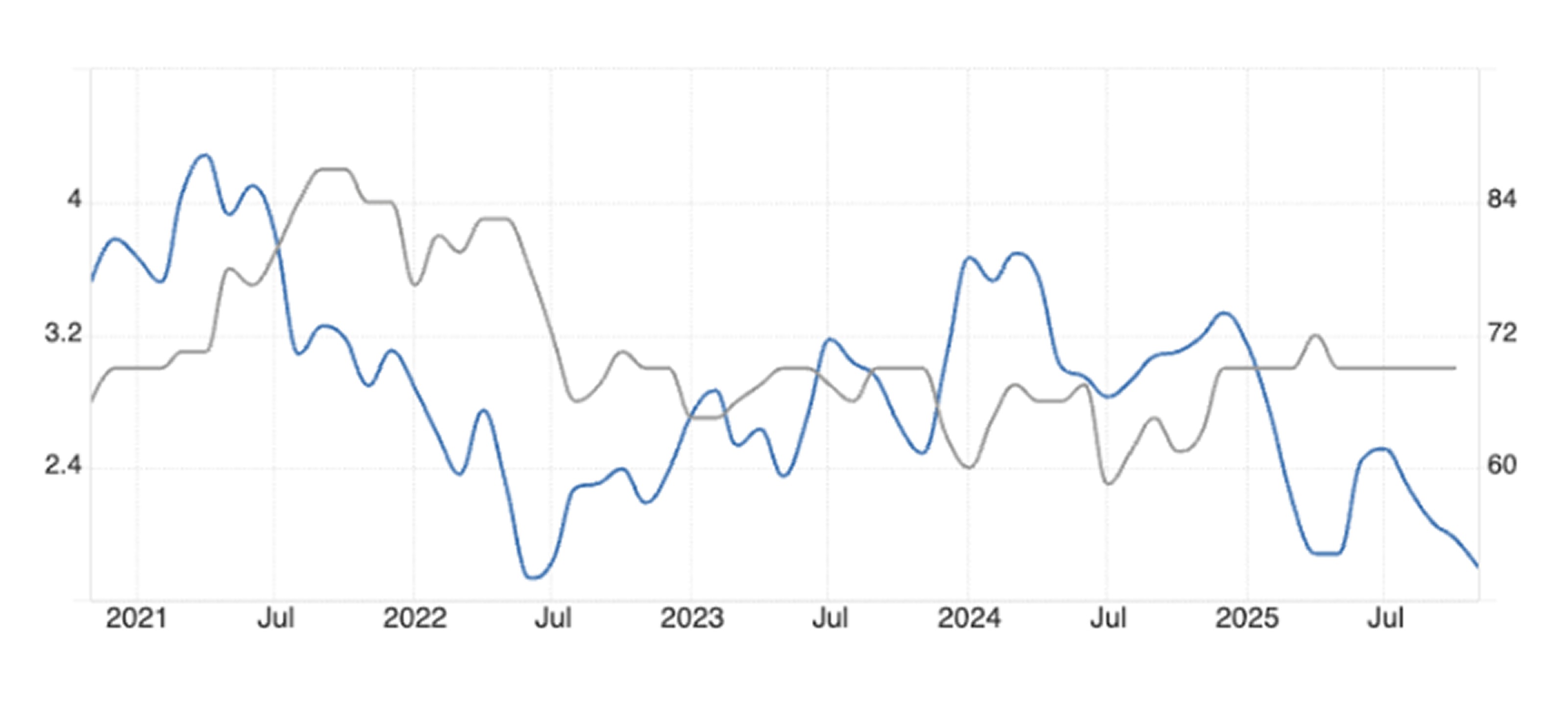

One of the most concerning signals remains consumer sentiment. According to the University of Michigan’s widely followed survey, the overall Consumer Sentiment Index edged up slightly to 51.0 in November from the preliminary reading of 50.3, supported in part by relief surrounding the end of the government shutdown (see the chart below). However, this slight uptick masks a deeper problem: confidence remains at the second-lowest level on record, just barely above the all-time trough seen in June 2022. The broader message is clear — American households remain under significant financial pressure.

The Current Economic Conditions Index, a measure of how consumers view their personal finances and present buying conditions, dropped sharply by 12.8%, falling to 51.1, the lowest level ever recorded in the history of the survey. The deterioration was broad-based, reflecting worsened assessments of household income, affordability constraints, and reduced willingness to spend on big-ticket items such as vehicles and household durables. These trends underscore a shift toward defensive consumer behaviour, with many households retrenching amid elevated borrowing costs and diminishing excess savings.

Outlooks for the future provided only limited comfort. The Consumer Expectations Index ticked up 1.4% to 51.0, but remains at extremely depressed levels consistent with recession-like sentiment. Interestingly, sentiment among wealthier households — particularly those with significant equity holdings — deteriorated late in the month, reversing earlier optimism. The decline aligns with recent market volatility and highlights growing concerns that slowing growth could spill over into corporate earnings and asset prices.

Inflation expectations offered a slightly brighter note. One-year ahead inflation expectations fell to 4.5% from 4.6% (see chart below)— the third straight monthly decline — while long-term expectations eased from 3.9% to 3.4%, a four-month low. Still well above Fed target rate of 2%.Although encouraging, these figures remain well above pre-pandemic norms and continue to complicate the Federal Reserve’s policy outlook. Policymakers are likely to welcome the directional improvement, but the persistence of elevated inflation perceptions reinforces the importance of maintaining credibility in the fight against price pressures.

US Consumer Confidence (blue)vs 3 Year Consumer Inflation Expectations(grey). Showing softening conditions whilst expectations on inflation remain elevated.

Beyond the consumer environment, business data pointed to a tentative moderation in growth. The latest S&P Global Flash Manufacturing PMI slipped to 51.9 from 52.5 — its lowest reading in four months — yet still remains above the 50-point threshold that separates expansion from contraction. Factory output growth remained positive but less robust, suggesting that recent tailwinds from a post-shutdown bounce may be fading. Meanwhile, employment within the sector rose at the fastest pace since August, indicating that firms are still willing to expand their workforce despite softer orders.

The deceleration in new orders may be the clearest warning sign within the PMI data. Weaker domestic demand has left several manufacturers more cautious in their production plans, particularly those exposed to discretionary consumer spending. However, longer supplier delivery times acted as a positive influence on the index — a development typically linked to increased activity levels — showing that conditions are not uniformly weak. Input inventories were largely unchanged, reflecting careful cost management amid uncertain demand visibility.

Wholesale inventory data also underscored the uneven recovery in business conditions. Inventories were flat month-over-month at approximately US$908 billion in August — a statistically neutral result but one that suggests firms remain hesitant to accumulate stock. Durable goods inventories increased slightly by 0.1%, helped by modest rises in metals, automotive and computer equipment. This was offset, however, by declines in key industrial categories such as machinery and professional equipment. Nondurable inventories dipped by 0.1% as chemical and pharmaceutical stocks were drawn down more aggressively, partially offset by gains in petroleum and agricultural products. On an annual basis, wholesale inventories rose 1.1%, signalling slow but positive inventory rebuilding compared to earlier estimates.

Taken together, these data points paint a picture of a US economy that is still expanding, but with growing signs of fatigue. Consumers remain severely pressured, confidence is sliding to historical lows, manufacturing momentum is slowing, and businesses are cautious in both hiring and stocking decisions. Yet, inflation expectations are easing, and employment indicators remain resilient enough to delay any sharp downturn.

This mixed landscape places the Federal Reserve in a difficult position. While the labour market and headline inflation trends suggest that a rate cut could soon be justified, ultra-weak consumer sentiment and fragile business confidence highlight the risks of maintaining restrictive policy for too long. Reiterates this view. Otherwise, the numbers are indicative of a consumer-driven recession, which we feel is highly likely. Market pricing currently indicates roughly a 70% probability of a December rate cut — a view bolstered by cautious commentary from some Fed officials — but divisions within the Federal Open Market Committee remain stark, as reflected in the minutes of the latest meeting. We will continue to support our bearish view for the time being.

A shortened Thanksgiving week in the US will likely see continued updates to the release calendar for economic data delayed by the recent federal government shutdown. Confirmed publications include producer prices, retail sales, durable goods orders, key housing price indicators, and regional business surveys for September. In the UK, Chancellor Rachel Reeves will deliver the much-anticipated Autumn Budget. Across Europe, major economies will release November inflation updates alongside confidence indicators for consumers and businesses. Inflation will also be monitored across Australia, Brazil, Mexico, Singapore and Japan — via Tokyo’s CPI print. Meanwhile, GDP figures are due from Canada and India, and the Reserve Bank of New Zealand will provide its latest monetary policy decision.

On the currency positioning front, we remain long AUD/USD and AUD/CHF, with both pairs showing strong potential to appreciate. This is becoming frustrating as the currencies seem locked to range. We will look to add to positions on a break above 0.6615 (AUD/USD) and 0.5310 (AUD/CHF). The EUR/USD position continues to perform well, and we are happy to hold. A break below 1.1470 would likely see further losses for the currency and more profit.

On the equity side, we have increased exposure at the beginning of the week, with the overall position showing profits.. We re-entered a short on the S&P at 6,894, which is already generating solid returns. We also opened a small position in gold at USD 3,977 with a stop at USD 3,850. Meanwhile, the wheat position — held as a climate hedge — is showing early signs of bottoming, reinforcing the resilience of the overall diversified strategy. We continue to hold these.